$TREC - Buyout coming in 2022?

Highly Attractive Execution Story in the Specialty Chemicals Space

Introduction

The Company I want to discuss today is Trecora Resources (NYSE: TREC), which is a US based producer of pentanes, hexanes and waxes. TREC is a relatively unknown $200mm market cap company that trades at a deeply discounted valuation, as the market is not giving the business credit for its true earnings power, due to a messy history of operational missteps. However, I believe the current setup is incredibly attractive, and shareholders are likely to be rewarded handsomely over the next 1-2 years, while taking minimal risk of capital impairment. The investment thesis is as follows:

Visibility to $40mm+ of EBITDA in 2022, which implies an EV/EBITDA of 4.8x, representing a significant discount to public specialty chemical peers trading at double-digit multiples

Change in narrative as historical issues are now all behind the Company (non-core asset divested, leverage reduced, new mgmt. team brought in, capacity expansions completed, and most operational issues resolved)

Strong downside protection from a pristine balance sheet, recent activist involvement, and an active share repurchase authorization

Business Overview / Company History

Trecora Resources is a leading producer of pentanes and hexanes in the US. The Company’s South Hampton facility is located in Texas, where the natural gasoline feedstock is processed into high-purity pentanes and hexanes through a distillation process. Pentanes and hexanes are generally used as processing aids, in applications such as blowing agent for foams, including polyurethane and polystyrene. Other key uses include being a condensation agent for polyethylene production, and a separation agent in the Canadian oil sands, where they are used to remove the asphaltenes from the tar. The Company does not disclose revenue split by end market or customer in detail, but ExxonMobil is the largest, accounting for 15% of total revenue. TREC utilizes both formula and spot pricing for products – and the formula is based on the average cost of the feedstock over the prior month, which helps smooth out the volatility from input prices over the longer term, but is still subject to a monthly lag.

The high-purity pentane and hexane market is a duopoly – with Trecora and Phillips 66 being the only players of meaningful scale, and TREC maintains a 60% market share. In the past, other players like ExxonMobil and Calumet Specialty tried to enter this market but ultimately failed – not only are significant capital investment and technical knowledge required, there are further barriers to entry from long customer approval timelines. This is understandable because pentanes and hexanes are usually a tiny (in terms of both volume and total cost) but crucial input component, and switching to a competitor product with lesser purity may jeopardize the entire process – which incentivizes the customer to stick with the incumbent supplier. All of this points to TREC being a high-quality business, but the issue is that hexanes and pentanes are by-products at Phillips 66’s refiners, and a rounding error for the consolidated operations, which means that there is a competitor with suboptimal price discipline. Therefore the margins for TREC are not perhaps representative of a typical duopoly, but nonetheless the Company has recently been successful at passing through multiple rounds of price increases, as demand recovers in the post-vaccine environment.

TREC also owns and operates a second plant in Pasadena, Texas, for its specialty waxes segment, which was acquired in 2014 for $73mm or 11.1x EV/EBITDA. Subsequently, the Company invested almost $50mm in cumulative capex to date, yet the segment has massively underperformed expectations due to challenging market conditions and a number of operational issues during the upgrades and capacity expansions which took place from 2015 to 2018. TREC faced a perfect storm of headwinds over the past handful of years, including similar operational challenges at the South Hampton plant, some end market softness (e.g. Canadian oil sands), impacts of COVID, and disruptions caused by cold weather in 1Q’21. However, there are much to be excited about the future, as most operational issues are now behind the Company, and TREC is well on its way to grow into the capacity expansions over the next few years. There is a new management team leading the charge, and the Company went from a highly levered entity to a net cash position from the sale of the AMAK subsidiary (a copper and zinc mine in Saudi Arabia) in 2020. Let’s dive into the investment thesis:

What is Normalized EBITDA?

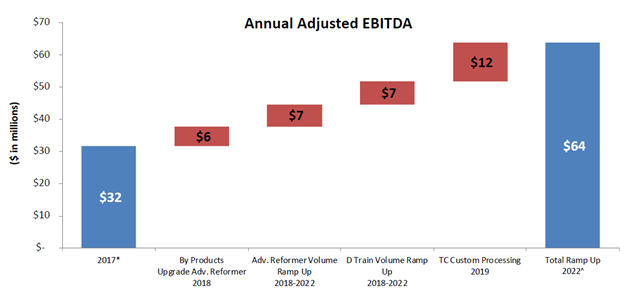

To value this business in a thoughtful way, it is crucial to figure out what normalized EBITDA should be. We should note that the company spent more than $100mm of growth capex during 2015 – 2018, so the equity definitely traded at times with some embedded expectation of future earnings growth. If we look at the 2018 investor presentation (now taken off the IR website), the old mgmt. expected the full run-rate EBITDA to be $64mm, to be achieved by 2022. Please see the bridge below:

Fast forward to today, it has become clear that the projections given by former management were wildly off the mark. It is out of scope for this writeup to go into every detail, but the Company faced several operational hiccups, project delays, end market softness (e.g. Canadian oil sands), unfavorable weather conditions, and of course COVID. It’s also probably fair to say that the original projections were overly optimistic as well. Thankfully, new management came in and reset expectations completely. Now the expectation is for TREC to do about $40mm of EBITDA for 2022 – and we know this because the Company did $31mm of EBITDA in 2019, and new mgmt. guided to $4mm and $6mm annual EBITDA improvements for 2020 and 2021 respectively through various growth projects. This is a far cry from $64mm originally anticipated, but I think mgmt. is being realistic, and perhaps sandbagging a little, to manage market expectations. Then there is spare capacity to fill beyond 2022 without spending any further growth capex, so theoretically EBITDA can grow strongly in 2023/2024 as well – but let’s not get ahead of ourselves, I do not like underwriting multi-year stories. But let’s not forget how cheap TREC is – if mgmt. can hit the $40mm EBITDA target in 2022, the Company trades for only 4.8x EV/EBITDA and a ~12% FCF yield on an unlevered capital structure – actually a tiny bit better because this includes a $6mm PPP loan that should be forgiven. This is ludicrous to me because specialty chemicals comps trade at double-digit multiples. If the upcoming quarters can show steady progression of tracking towards this FY’22 EBITDA target, I believe the rerating will be fast and furious.

Management & Capital Allocation

It’s worth talking about management in more detail because this is an important part of the narrative. The C-suite has gone through a complete makeover, with the CEO, the CFO and the CMO all being new to their positions – as of 2018, 2021 and 2021 respectively. The old guard has taken responsibility for the historical underperformance and left, and we now have fresh eyes looking to make changes for the better. Patrick Quarles, the CEO, has an impressive background, with senior leadership experience at much larger organizations such as Celanese and LyondellBasell Industries. But I find it more compelling that he wasted no time buying up shares in the open market, to the tune of $1.4mm dollars in aggregate, at an average price of $7.79/share (and $1.0mm of this was purchased pre-pandemic, at an average price of $9.56/share). $1.4mm is more than his annual cash compensation (base plus bonus), so even for him this is a decent chunk of money, and speaks to his confidence in the go-forward plan.

I also like the fact that the Company has a new $20mm share repurchase plan authorized as of March 2021, which could reduce share count by 10% upon full utilization at current share prices. The Company has already repurchased 88,000 shares in March at an average price of $7.86, with the commentary that the program “continues into the second quarter”. An encouraging sign in my opinion.

Activist Involvement

Let’s take a brief pause. I think Trecora is an interesting investment for reasons explained above. However, I would not be writing this up for subscriber consumption if that was all there to it – sure we have the “steak”, but there simply isn’t enough “sizzle”. But have no fear, there is a sexy angle here from an activist shareholder being involved.

The firm is Ortelius, an NYC based activist fund, which has amassed an 11% stake in the Company. Notably, Ortelius has been purchasing stock in the open market as recently as 7/12/2021, at $8.27/share (4.4% higher than close on 7/30/21). So they may well still be in the process of accumulating shares for their desired position size, which creates a positive technical.

Unfortunately I was not able to reach Ortelius to discuss their investment in TREC, but I think their motives are fairly obvious. We have a highly undervalued company in the middle of a “show-me” execution story, trying to profitably grow into the capacity expansions already built out. If TREC is successful, then the stock price will react appropriately, in which case Ortelius should be able to exit over time and generate a stunning return for themselves.

On the other hand, if the new mgmt. team fails to execute, then Ortelius would promptly push them to sell the business. In fact, I would claim that Ortelius has already backed itself into a corner – because when you build a 10%+ position in an illiquid microcap, it is virtually impossible to exit in the open market without taking a massive loss. If an activist firm with a material holding decides to dump shares, this is 1) a condemnation of the fundamentals from a very sophisticated investor and 2) a horrible technical as they would need at least 3-4 months to exit, assuming they can execute sales at 25% of daily volume. This gives ample opportunity for savvy holders to front-run them, which can potentially cause a death spiral for the stock price. Now, I think this is extremely unlikely to happen, because the team at Ortelius are presumably smart guys and won’t shoot themselves in the foot – rather they will push to sell the Company, and I believe that there will be unanimous support given the long history of suffering shareholders. No management or board member would dare oppose this motion, as they will simply be replaced at the earliest convenient opportunity.

Finally, there is another interesting value-creation angle here, as the Company could potentially sell off the wax business. The Specialty Waxes segment has its own plant in Pasadena, so I don’t think there would be huge dis-synergies if this was spun off or sold to a strategic. Remember that TREC bought this plant for $73mm back in 2014, and has subsequently invested almost $50mm in capex, much of it for expansions and upgrades. I believe the Company is getting almost zero credit for any of this creation basis in today’s stock price, so if they were able to sell the waxes business for even a fraction of the replacement value (perhaps as low as $50mm) then we can create the core Specialty Petrochemicals segment for an outrageously low multiple. This would be an easy value-creation lever if push came to shove, and Ortelius may opt for this solution if there is a reasonable bid for this asset.

So how might this story play out? Well, I think that the activist will push for a sale eventually regardless of financial performance – but the timing of it is very uncertain, and it all depends on their patience, or lack thereof. As a base case I can imagine something like this – TREC hits $40mm of EBITDA in 2022 (actual or run-rate) and then puts itself up for sale, and then Private Equity buyers can probably underwrite to $45mm of transaction EBITDA based on removal of public company costs and corporate fat trimming (and they will hire a consultant to make up numbers if they have to). I think TREC works really well as a PE LBO, and can easily provide 20%+ equity IRRs for the buyer under conservative assumptions. Here’s my straw-man model:

Concluding Thoughts

Let’s bring it all together. I believe that Trecora is a compelling execution story with a lot of embedded fundamental upside from EBITDA growth, but the strong downside protection ultimately won me over. Not only does TREC trade at a significant discount to public comps and replacement value, the Company has a pristine balance sheet in a net cash position. If that wasn’t good enough, there is an activist running around hoovering up shares, and a share repurchase program in place actively being utilized.

It is difficult to conceive of a multi-bagger outcome with an unlevered balance sheet, but I am more than willing to take the trade-off because I see very little downside here except in the most draconian scenarios. I see 50-70% upside in a year with potential for superior returns if EBITDA growth surprises to the upside, or if strategic alternatives are forced upon the company earlier than we expect. I have made TREC into a core position, and believe this is a good candidate to average down if the near-term trading is choppy for whatever reason.

Disclosure

Plum Capital is long TREC Common Stock

Note – Trecora is reporting earnings after market close on August 4th. I am not expecting fireworks for 2Q either way, but please be warned that the stock may experience volatility typical of earnings announcements.

Pangaea Ventures/Ortelius Advisors us a recent holder. From our conversations they're not looking to sell the company.

Plum - I found this comment attached to a Value Investors Club article...

Mitc -

Thanks for the refresh - great overview of what has gone wrong and the potential for what can go right. We've followed TREC for a better part of the decade, maybe a couple years after Simon came in, but haven't been close to it for a while.

A few thoughts. Although TREC isn't a pure commodity chemicals company, it does seem to us to be in between that and "true" specialty chemicals.

For example, we followed (and briefly owned) KMG, which (as we recall) had much higher margins and returns... their wood business was "meh" as far as growth but the semiconductor chemicals (and then Flowchem) were clearly very solid and differentiated businesses with growing end-markets. And then you have AXTA in the comp table, which is paint, which is clearly a very, very different business with different characteristics such as very strong cash flow (this was well-covered on VIC a few years ago, so we won't go into it - just pretty obvious that AXTA and TREC are not comparable).

At TREC, the most identifiably differentiated piece is the high-purity pentanes - but as you pointed out, oil sands are a big customer here, and once that buildout ended, their growth here has really stalled out, and it's not clear that there are lots of applications that will drive meaningful volume growth. Moreover, duopolies generally tend towards strong pricing and rational behavior, but our understanding from over the years is that it is such a small piece of Phillips' business that they occasionally do strange/crazy things, which keeps a lid on pricing.

Finally, TREC's results tend to be whipsawed a bit by commodity pricing (advanced reformer was supposed to help here but has been challenging so far.) And if you buy the near-term secular-decline thesis for oil (we don't, but clearly the market does), then there is sort of double exposure to commodity prices, and it is hard to think this business will garner a really high multiple?

Maybe we don't have enough insight into the waxes, but considering that this has probably been the single most disappointing part of their business (it was struggling since well before the advanced reformer headache), it's also not clear that it deserves a premium multiple until they have several years of consistent execution and strong margins under their belt. We understand wax is sold out now, but demand dipped during the initial COVID lockdowns, so downturns in certain end-markets could certainly change that pretty quickly. What are the real barriers to entry here? What are TREC's advantages?

And then there's capital. Management has cited $10-$11MM as pure maintenance capex (see Q2 2019, Q3 2020 call). This is heavy equipment subjected to heavy loads. This is a pretty significant burden on $40MM EBITDA that you forecast, especially considering how new much of their equipment is. Again as comparison, looks like KMG's capex in their last year before the buyout was $25MM on $120MM of EBITDA, or the same ratio, but this included an ERP implementation as well as expansion of their facility in Singapore, so the pure maintenance number was perhaps $15 - $20MM? So to compare KMG's multiple, you have to take into account that they were doing at most 2x the maintenance capex on 3-4x the EBITDA, not to mention the better margins, growth, end-markets, etc.

Of course, if TREC manages to fully utilize all the growth capital, then their EBITDA will rise and capex will be a proportionately smaller burden, but I think part of the problem here is that even ex growth capex, the company has not generated a lot of FCF.

It is clear that they have under-executed (and had lots of bad luck) over the past 5 years, and it does seem very likely that they can improve their results meaningfully just via basic blocking and tackling, which would hopefully result in a higher stock price. But the assumptions required for a $20 stock price in one year seem very aggressive to us - perhaps 3-5 years down the line with strong execution (which of course would be a great IRR from here). What do you see differently?