Plum Capital post #2: Jakks Pacific (NASDAQ: JAKK)

Get ready for Halloween - On a Sunday!

Housekeeping

Dear subscribers – thanks for signing up! And for the US subs, wishing everyone a happy July 4th weekend.

I plan to use this Substack solely to post my highest conviction pitches or the most interesting ideas that I find in the markets at any given time. I deeply respect everyone’s time, and don’t want to dilute the experience by discussing second or third tier ideas. I like big double/triple digit returns (who doesn’t?) and will not bore you with names that I think are mispriced by 10-20%.

Having said that, please consider following me on Twitter (@Plum_Capital). I will have more to offer, it’s sometimes fun to explore extra ideas that won’t quite make it to the Substack, or discuss finance topics more generally. And if you have enjoyed my first couple posts, I’d appreciate any referrals to friends or colleagues! I have many more ideas in the pipeline, and I am optimistic that I can create a lot of value for my subscribers. Now let’s get back to the regularly scheduled programming.

Introduction

We all know that the “reopening” theme has played out to a large extent, particularly in the US market. In many instances, former COVID-losers are trading far in excess of pre-COVID valuations, be it cruise lines or movie theaters. There are several potential reasons as to why such businesses may have become more valuable in a post-vaccine environment in the eyes of the market – pent-up consumer demand, leaner cost structures, competitors exiting the market, and so on. But the equity markets remain frothy, and we are in a challenging environment for deploying excess capital.

However, if you look in the small-cap and micro-cap world, there are many businesses continuing to trade at bargain basement prices, even though they are subject to the same aforementioned tailwinds as their larger cap counterparts. This valuation discrepancy is easily explained in most cases – often driven by liquidity reasons or lack of market awareness (limited sell-side coverage, etc.). The opportunity here is that the rerating can be explosive when the improving fundamentals finally hit the market over the head, which means that investors who recognize these setups early can be rewarded swiftly.

I believe that Jakks Pacific (NASDAQ: JAKK) is one such example. JAKK is a manufacturer and distributor of toys and costumes, with presence in the US and abroad. The Company should more than double EBITDA in 2021 on a YoY basis, as the pent-up demand drives incremental revenue, which will flow through on a greatly reduced cost structure. The market is completely asleep at the wheel, valuing this business at 3.3x EV/EBITDA and 28% levered FCF yield to Equity on 2021 numbers. However, this is not the end of the story – there are several idiosyncratic reasons why I believe JAKK is a superior investment versus other reopening plays:

1) JAKK is highly seasonal, and generates all annual EBITDA in 3Q, as retailers stock up prior to Halloween and Christmas. I expect 3Q’21 to be a blow-out of epic proportions, driven by pent-up demand as the vaccinated US population looks forward to Halloween festivities

2) This is a short duration idea, with bargain basement valuation providing downside support. If the thesis does not pan out, your capital can promptly be redeployed to other opportunities

3) The Company recently executed a successful refinancing transaction, which reduced the cost of debt by 300bps. Additionally, the outstanding Convertible Notes will convert to Common Equity by September, further simplifying the capital structure. I believe the market has not appropriately repriced the equity, and the resulting increase in FCF will be evident in the coming quarters

Business Overview

The business model is easily digestible. The company designs, manufactures and distributes toys, costumes, electronics and outdoor furniture. In most instances, the Company enters into a licensing deal with the content creator / IP holder such as Disney, and creates associated toys and equipment (e.g. a character action figure from a recent movie). Royalty payments range from 1-25% of revenue, sometimes with minimum guarantees, and is a key cost bucket above gross margin. All manufacturing is done in China by 3rd party partners, and finished products are sold to retailers or distributors. The customer base includes mass market (Wal-Mart, Target), specialty retail (TJ Maxx, Ross Stores, GameStop), big box retail (Costco, Sam’s Club) and dollar trade (Family Dollar, Five Below). Wal-Mart and Target are the biggest customers, accounting for 29% and 25% of revenue, respectively.

The toy industry can fairly be described as a competitive one. Hasbro and Mattel are by far the largest players, with tremendous scale benefits and vast collection of IP owned in-house. Therefore the two giants enjoy market leading EBITDA margins, typically ranging from 15-20% depending on the the company and the year. Then there is a long tail of smaller competitors, of which JAKK is one of the more notable players. In this regard, it is worth mentioning that JAKK’s business strategy is focusing on product niches that Hasbro and Mattel don’t have a big presence in, whatever the reason may be. More importantly, both the content creators (i.e. the Disneys and Warner Bro’s of the world) and the major retailers do not want the toy industry to be a duopoly, thereby giving Hasbro and Mattel all the bargaining chips at the table. So there is a reason for smaller operators like JAKK to exist, and the relationship is valued by other participants in the supply chain. Interestingly, JAKK also licenses certain products from Hasbro and Mattel, which means that there is some level of cooperation and goodwill between the entities, and not just pure competition.

Finally, JAKK is a toy manufacturer that is highly focused on Halloween sales. Naturally, you would expect all toymakers to have a strong 3Q as retailers stock up for Halloween and the holiday season, but JAKK’s financials are particularly seasonal, with all the EBITDA being generated in 3Q, and other quarters running at breakeven or at a loss. This is a key observation that will become important in my thesis.

Pent-up Consumer Demand and Halloween in 2021

2020 was a disappointing year for US partygoers, as certain lockdown measures were still in place, and the general fear of large gatherings was still quite prevalent last year during Halloween (recall that this was before the groundbreaking news of Moderna vaccine efficacy data in November). With the fully vaccinated population growing by the day in the US (almost 50% of total US as I write this), I believe that there is a good chance that Halloween festivities are off-the-charts this year, with both adults and children sick of being holed up indoors for the better part of the past 18 months. This obviously bodes well for the sale of toys and costumes, but if that wasn’t good enough, Halloween falls on a Sunday this year, a fact that mgmt. stressed several times in prior earnings calls:

This is important, because as mentioned before, 3Q is the most consequential quarter in the year. 3Q is going to make or break the performance for FY’21, and I expect the pent-up consumer demand to really make a difference given that 3Q’20 had revenues falling off by 14% due to the pandemic. The film slate and the associated product offering isn’t too shabby this year either, with Raya and the Last Dragon being quite popular, and Encanto coming up later this year (admittedly a 4Q impact for the latter).

Impact of Cost Savings

As we all know, revenue is only half the equation and we must discuss the cost structure before coming to any conclusions about profitability. Thankfully, management has done a great job of cutting cost during 2020, setting up for margins to explode this year when incremental revenues flow through. The company had a pre-existing cost structure review with a 3rd party consulting firm prior to COVID, but the pandemic accelerated and increased the scope of the cost initiatives, with expenses being slashed across the board. As a result, FY’20 gross margin expanded by 240bps despite a 14% decline in revenue, and SG&A was reduced by $26mm (or 16% YoY), reflecting significant fixed cost takeout.

So what will happen to this business when topline returns to growth, given that so much of fixed costs have been removed? Well, we already had a sneak peak from 1Q’21 results. Revenues increased by +26% YoY, which was remarkable as the Company outperformed despite having no benefit from a blockbuster theatrical release. Given the lowered cost structure, EBITDA increased by a whopping +$12mm, from ($14mm) to ($2mm). The significance of this YoY move is easily understood, when we consider that FY’20 EBITDA was only $28mm (i.e. LTM EBITDA changed from $28mm to $40mm in just one quarter!). This is particularly encouraging because 1Q is typically the weakest quarter in the year, a fact that the Company wastes no time pointing out in the filings:

Base Case 2021 Projections

I believe that now we have all the necessary tools to take a crack at 2021 projections. It’s in my DNA to be conservative when doing any numerical analysis, so I’m going to make a fairly punitive assumption off the bat and grant very little EBITDA improvement in both 2Q and 4Q this year. I would not be surprised to be proven wildly incorrect (in a good way) but at least it gives us some margin of safety.

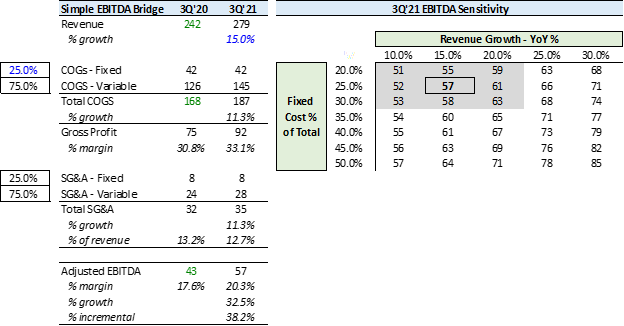

So then, let’s dig into the all-important 3Q. I am comfortable assigning a +15% revenue increase, to get us back to 3Q’19 level of topline. Again, I wouldn’t be surprised to see the pent-up consumer demand getting us past that level, but I don’t want to make any herculean assumptions. With respect to the cost structure, I do not believe that mgmt. has ever publicly disclosed the fixed vs. variable split, but we can make an educated guess given our understanding of the business. I believe that the cost structure is largely variable, as manufacturing costs and royalties, as well as marketing and other direct selling costs should be predominantly variable. However, there are some chunky fixed cost line items too, such as operating leases, corporate and G&A. After reviewing the filings, I am happy with assigning a 25/75 fixed/variable split for the purposes of our analysis. This results in the following table, and $57mm of estimated EBITDA for 3Q’21. Bringing it all together, I arrive at $56mm of EBITDA for FY’21.

Thoughts on Valuation

I think that a ~5.0x multiple is easily justified on 2021 EBITDA of $56mm, based on a conservative DCF, even if we believe that 2021 is somewhat of a peak year in terms of profitability (i.e. 2022+ Halloween trails off a bit, and fixed costs creep back to a certain extent). We can also examine LFCF yield on the equity, which comes out to be around $31mm excluding working capital movements ($56mm EBITDA, $12mm capex, $7mm cash interest, $5mm cash taxes). This equates to a 28% yield on pro-forma market cap of $110mm, which to me implies that the equity is outrageously mispriced at current prices. If we grant the 5.0x multiple, there is more than 100% upside in the stock.

As hinted at earlier, I say pro-forma market cap because I am reflecting the impending conversion of all Convertible Senior Notes to equity, as the maturity is in September this year and the Notes are well in-the-money. With that in mind, please refer to the below snapshot of the capital structure to help visualize how cheap JAKK is trading right now. 3.3x forward EV/EBITDA is simply too low in my view.

Potential Pushback

One potential pushback I can imagine goes something like this: “2021 might be peak earnings, so why should we give credit for multiple expansion on $56mm of EBITDA?”

I have given this a lot of thought and here is how I justified the investment in my head. I think my thesis was constructed in a conservative way, so if I am wrong then there is limited downside, and there could be a ton of upside if I am proven to be correct. Also, I do simply think that literally no one is paying attention to JAKK (save for some motivated retail investors here and there), so the market is in automatic “show-me” mode until quarterly earnings hit, upon which I expect the market reaction to be swift and violent.

Finally, even if I am wrong, let’s not forget that the Company will generate a LOT of cash if EBITDA is anywhere near $56mm for FY’21. Mgmt.’s capital allocation priority is paying down debt (the Benefit Street Term Loan is priced at L+650 with a 1% floor, which mgmt. deems as expensive), and if they follow through with that plan, the Term Loan balance will be significantly lower at the end of the year. I think there is some possibility that the market narrative on JAKK changes at that point, from a highly levered subpar business to a decent, moderately levered company that throws off a lot of cash. The ugly duckling doesn’t need to turn into a beautiful swan, merely growing up to be an average looking duck would get us paid handsomely here, in my opinion. I am personally targeting at least a double here from the current stock price.

Disclosure

Plum Capital is long JAKK common stock

Dear subs - I have been getting a number of inquiries regarding the large trading volume today and the significant intra-day volatility. In short - I am not sure, but it could be 1) holders of existing convertible notes converting into equity and selling in the open market, or 2) short-term driven traders taking advantage of the recent rally to sell down. As for me, I am in this to see my thesis play out over the next 4-5 months, not sell out for a quick buck. Of course none of this is investing advice, and what any individual subscriber does is out of my purview, but just wanted to put this out there to pre-empt further questions regarding this topic. FWIW, I've personally had better results historically by being patient with my positions, rather than trying to frequently trade in and out of them and "timing the market"

nice post. Have read similar view in seeking alpha at a slightly lower price point. Two stocks with equal or lower valuations are CATO and DXLG yet completely different stories. Seems JAKK is more of short term play. Good idea.