Housekeeping

Dear Subs, I had the intention of releasing a juicy new idea by Friday, but there were several developments worthy of an email update for the existing ideas (JAKK and IEA). I had to re-prioritize given the urgency of the news, and therefore the new idea will probably be released early next week, to give myself ample time to tighten up the pitch.

Going forward, my hope is to generate at least one thoroughly researched idea per month, and follow up with additional emails if there are material updates to existing ideas. I think this is a low enough bar for me to step over, so you should expect that level of formal interaction from me on Substack.

But that isn’t to say that you can’t connect with me via Twitter, the comments section or my email on Plumfamilyfund@gmail.com. I love it when subscribers reach out to dig deeper into my writeups or discuss completely new ideas, so if you ever want to talk, don’t hesitate to reach out. I will respond to all serious inquiries within a day or two, if not earlier.

Finally, if you’ve gotten any value out of my ideas or just simply enjoy reading the pitches, please refer this blog to others! There is no paywall here, and I’d like to build a bigger following so I can have more meaningful interactions with like-minded investors – this should all accrue to better idea generation in the future.

JAKK Update – 2Q’21 Earnings Summary

For the TL;DR crowd – I did a short Twitter thread, please check that out instead if you prefer

What can I say… the earnings were a complete blowout. Here’s a quick summary of all the salient points:

Revenues up +18% compared to 2Q’19 (more appropriate comp vs. 2020 given COVID)

Adjusted EBITDA of $5.0mm vs. ($4.6mm) prior year

LTM EBITDA increased from $39.5mm to $49.1mm

Management thinks they are on track for a “great Halloween season”

Convert overhang mostly removed as only $2.9mm face value of Notes remain

Inventory level increased to $60mm, slightly ahead of historical June 30 levels

To be fair, there were some risks addressed on the call as well – mostly to do with supply chain disruptions and increased transportation costs. Mgmt. cautioned that this will likely be a headwind in 2H’21, without giving any quantitative guidance for the impact. However, we should note that these concerns were very much present for most of 2Q as well, and yet the Company printed an amazingly strong quarter. It’s often dangerous to extrapolate, but I suspect that this is small potatoes vs. the Halloween related 3Q demand and the overall impact of cost cutting achieved to date. So I don’t think it breaks the thesis.

Now recall that my expectations for 2Q were pretty low – in fact, I had penciled in $0mm EBITDA for the quarter in my excel model purely for conservatism. However, given this strong showing, I now believe that FY’21 EBITDA may fall between $60-70mm, if the Company can continue to execute in 3Q and 4Q. Updating my numbers for the quarter, this implies that JAKK is currently trading at ~3.3x EV/EBITDA based on $65mm of “new base case” EBITDA for 2021. This is far too low, and I continue to believe that the stock belongs in the low $20s, if not higher. As the buyside accounts digest the numbers and update their models, they will realize how cheap this is, and many would get off the sidelines, in my opinion. There could also be a potential catalyst if any sellside firm upgrades JAKK based on improving fundamentals.

Finally, I’ve been getting a LOT of questions and comments in regards to the high volatility in the share price. I already addressed this, and I continue to believe that this was mainly due to the Senior Note conversions and holders selling stock in the open market. But a few people have alerted me to another factor that may well be real – so a quick paragraph below to explain:

It has come to my attention that the above Twitter account has been posting various bullish tweets regarding JAKK. It also appears to me that this individual has not done any real work (or at least has not published it in the public domain in an accessible manner) but continues to chirp away with random, unsubstantiated snippets of info, claiming that the stock is attractive. Again, I don’t want to comment on this in depth, but anyone with 200k+ followers has potential to move a stock if enough people decide to blindly follow their lead. I suspect this added a material number of retail speculators into the mix, which can lead to choppy trading as people try to “time the market”. This behavior appalls me – most retail investors should not be rampantly speculating in the stock market (there is no edge there and most people end up losing money over time) but hey I don’t make the rules, and I am not responsible for how anyone else trades with their own money. My strategy is to play the longer term “buy and hold” game and wait for the thesis to play out, ignoring all the noise in the interim. I hope my subscribers generally agree with my approach.

I will close by saying that I am very encouraged by the 2Q results, and have added some more JAKK shares in after-hours trading. Bring on 3Q earnings – only 3 more months to go!

IEA Update – 2Q’21 Earnings Summary and Recapitalization News

One of the best feelings as an analyst is when you absolutely nail a thesis, regardless of whether you make money or not, because at least you know that your investment process and analysis have been sound. And I know very well that you can make the right fundamental call and still lose money, so the jury will be out for a while with this one.

So let’s dive into it. 2Q earnings were fairly in-line with expectations so I won’t say too much here. Admittedly there were some unfavorable YoY comparisons (e.g. EBITDA for the quarter was $35.7mm vs. $39.3mm prior year) but this doesn’t really mean anything because it was driven by timing of various projects. Notably, mgmt. reaffirmed revenue and EBITDA guidance for 2021 – so they are confident that they can hit the targets. Also, the Company reported a backlog number of $2.8bn, which is another all-time-high, certainly a good fundamental sign. IEA will hold an earnings call on August 10th, so we will learn more then.

More importantly, the Company announced a global refinancing of the capital structure, very much in line with how I described it in my IEA writeup on July 15th. There is a lot going on, so please refer to the below – and note that certain numbers are still subject to change.

Transaction Components

Issuance of new Common Stock

Full conversion of Series A Preferred into Common Stock

Full redemption of Series B Preferred and payment of redemption premium

Issuance of new Revolving Credit Facility

Issuance of new HY bonds

Refinance existing Credit Facility

Payment of fees & expenses in connection with the above transactions

Potential use of B/S cash and/or proceeds to B/S in connection with the above

Sources & Uses (Not Final and Subject to Change – Plum’s Straw Man)

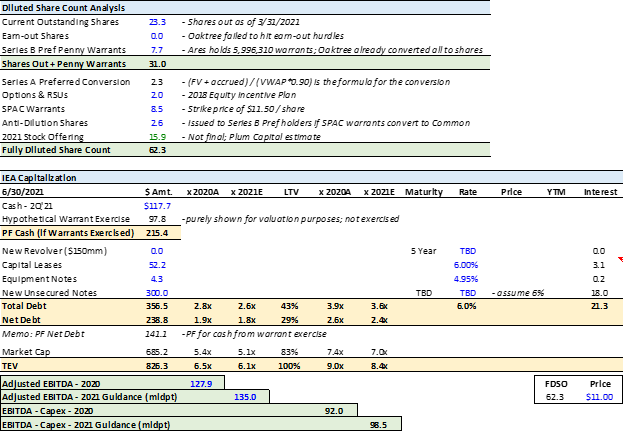

I’ve also updated the capital structure, PF for all the new developments that we have learned about. Now please go back and compare this with the capital structure that I’ve laid out in my old writeup – truly a massive simplification! While there are still plenty of nuances, this is much closer to a traditional cap stack than the Frankenstein’s monster that we had before. I see this as a material breakthrough.

I don’t like hiding relevant information, so I’ll admit that there are some drawbacks here – the obvious one is the dilution to the share count (it is what it is) and you will also see that the EV/EBITDA has crept up by 0.3x as a result of paying the redemption premium and the fees associated with the transactions. However, what is encouraging is that the Company got a significant discount on the redemption premium (it was 1.5x min MOIC but they are only paying $48mm; I expected closer to $80mm so Ares must have agreed to give IEA a hefty discount to get this deal done).

Finally, the language in the offering docs implies that Ares will take down a significant percentage of the offered shares – such that their PF ownership of the Company may exceed 37.8%. I think this is a great sign, because Ares must have conducted open-kimono private-side diligence of the company over the years as part of its Preferred investments, and came to the conclusion that owning more of the Common Equity is attractive enough to agree to this deal. I know Ares well enough to say that they are a very sophisticated firm, and no doubt decided this after thorough diligence and having gone through their Investment Committee process. Of course this means absolutely nothing at the end of the day (remember Lynch said that the smartest investors on the planet get 4 out of 10 wrong!), but it is still nice to have that institutional seal of approval – certainly is good optics as more prospective investors sharpen their pencils on the stock, now that the “complex capital structure” overhang is going to be removed in short order.

I am pumped that this process came about so quickly – I had initially imagined (as suggested in my old writeup) that cleaning up the cap stack may take as long as 18 months. Given this positive development, I have meaningfully added to my position in the after-hours trading on the 28th. I suspect that as this news gets digested across the buyside and the retail outlets, light bulbs will start to go off and more investors will be attracted to the story. Finally, with the new infrastructure deal looking to pass the Senate, there is continued macro momentum here and I am very excited to see the art of the possible in the next few years. My price target remains the same, I expect a double from here to be quite achievable in the next 12-18 months if the Company continues to execute.

Disclosure

Plum Capital is long JAKK and IEA Common Stock

Oops, info already stale. They priced $175mm offering today at $11. I was being too conservative by assuming $10. Even better!

Thanks a lot! I appreciate your work!