$IEA - Plum's Favorite ESG Play

Macro Tailwinds Present Massive Opportunity

Introduction

I am bullish on commodities, and recently had my “priors confirmed” with oil breaking $75/barrel. I wanted to find an actionable idea, and had a light bulb go off – if oil prices keep skyrocketing (highly debatable, but stick with me), I think that renewables become an extremely interesting proposition. Mind you, wind and solar have come a long way, through technology and engineering improvements (more efficient blades and panels, for example) but now just became 50% more cost competitive when oil went from $50 to $75/barrel! No need to state the obvious, but the math may even approach no-brainer territory if oil breaks triple digits.

I got excited and revisited a name that I have studied for a long time – Infrastructure and Energy Alternatives (NASDAQ:IEA), an EPC company specializing in wind and solar projects. I have concluded that IEA is one of the most attractive ways to play the ESG game, for the following reasons:

Tsunami of macro tailwinds – ESG, favorable legislation, infrastructure bill and high oil prices

Growth company trading at a depressed value multiple, at a discount to generic EPC comps

Refinancing catalyst in the not-too-distant future

Downside support from strong FCF generation and low entry valuation

Business Overview and Company History

IEA is an EPC business specializing in renewable energy, with some civil exposure gained through acquisitions. Put simply, they take care of the construction and installation of wind turbines and solar panels for large scale utility projects, and their customer base includes all the tier 1 renewable energy developers (Exelon and Nexteras of the world). IEA was formerly an Oaktree portfolio company, but went public through a SPAC deal in 2018 as a pure-play renewable EPC serving the wind and solar markets. IEA subsequently diversified into additional end markets such as civil (roads and bridges) and rail, through two meaningfully sized acquisitions which closed in 2H’18.

The industry is dominated by a few large players, including IEA, Blattner Energy, Mortenson, Bechtel, and Kiewitt. Some of the larger public EPCs used to have a presence as well, but since have exited, and a longer tail of smaller operators rounds out the rest. While it may not be obvious from first glance, this is a reasonably competitive industry, as you are dealing with large, sophisticated utilities on the other side, who go wide with RFPs – resulting in competitive bidding processes. Utilities tend to run with tight budgets and try to limit the construction costs to about 30% of the total project capital spend, so it has historically been tough for EPCs to expand project-level margin, even for best-in-class operators like IEA.

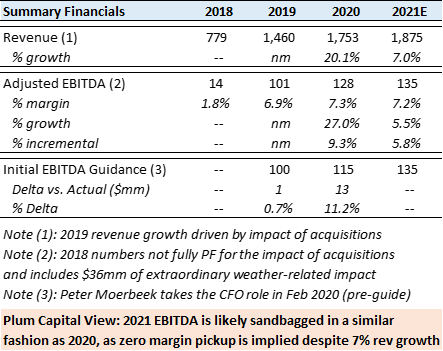

Very briefly on IEA’s historical performance – the Company woefully missed guidance in 2018, in its maiden year as a public company, due to extreme weather conditions in the 4th quarter in most of its key markets. Torrential rain disrupted multiple projects, leading to unplanned labor and equipment costs. This was almost a $40mm drag on EBITDA, a horrific result given that full year guidance called for $120mm of PF EBITDA at the midpoint. The Company faced a liquidity crunch and had trouble managing debt covenants, so they had to resort to an expensive rescue financing from Ares, in the form of Preferred Equity. This sequence of events led to the stock falling by more than 80% in less than a year. However, the Company subsequently regained its footing and started executing again, with strong results in both 2019 and 2020 – a quick summary table is provided below:

Macro Backdrop

Let’s start with the macro, because I think it helps frame the rest of the discussion. My longer term thesis is pretty simple, that oil prices will remain elevated, as the supply side is pressured by ESG initiatives and lack of investment, while demand increases further from all economies eventually recovering from COVID. Not only do renewables become directly cost competitive, wind & solar will benefit massively from ESG and regulatory tailwinds. The icing on the cake would be the passage of a new infrastructure bill, which would further boost the civil side of the business as well. And we shouldn’t forget about the fresh capital pouring into ESG funds being raised at all the large asset managers – the macro backdrop cannot be more positive for companies like IEA right now. Management is well aware of the industry tailwinds, with some detailed commentary provided in the most recent earnings call:

Valuation Framework

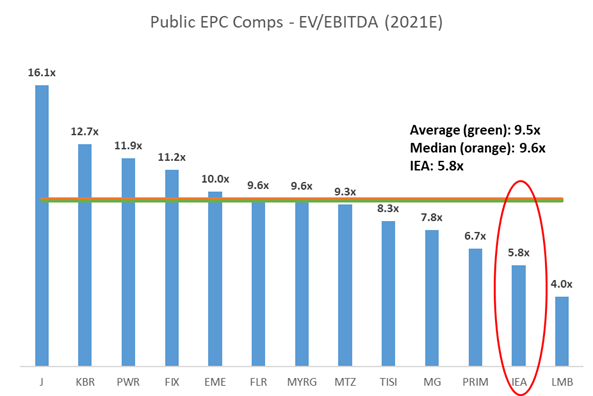

The macro picture looks promising, and IEA seems to be in the right place at the right time – so let’s turn to valuation. IEA is trading at a meaningful discount to generic EPC comps, and absolute valuation is quite palatable as well. Please take a look:

Few observations from these charts – IEA has middling margins, but trades at by far the lowest valuation of the bunch (only Limbach is cheaper – but that is a subscale comp with a very messy history). I think this is ridiculous, because no other comp on this list has the same level of organic growth potential or ESG related tailwinds as IEA. We must respect the fact that some comps have higher margins, comparative scale benefits, and an established track record of performance, so I am not saying that IEA deserves a market-leading multiple. But more than 3.5x turns of discount for IEA from the comp median is grossly unfair, in my view.

Capital Structure Overhang – Leads to a Refinancing Opportunity

So what exactly is the problem, you may ask. I am not going to bury the lede, IEA suffers from a valuation discount because the capital structure is a giant mess. Fortunately, Plum Capital has done all the heavy lifting, so all you need to do is appreciate the complexities here:

Are we having fun yet? Don’t worry if any of this is too complex – the main takeaway is that IEA is currently trading at 5.8x EV/EBITDA based on mgmt. guidance for 2021, if we account for all potential forms of dilution to the share count. Now the problems should be obvious to you – 1) the capital structure is horribly complex (and the market generally hates complexity) and 2) Preferred Equity has a high dividend rate, which detracts from the true FCF potential of the business.

Unfortunately, fixing this capital structure is not a trivial task. The Preferred was placed as a rescue financing after the disastrous outcome in 2018, and as such has a high cost of capital and restrictive call protection. In fact, the Series B Preferred is guaranteed a 1.5x minimum MOIC if the paper is to be refinanced – which prohibits an immediate takeout as the Company would be on the hook for almost $80mm on top of the face value and the accrued amounts. But is all hope lost until the Series B Preferred is mandatorily redeemed in 2025? My answer is no, I think there is a viable path for a refinancing if the Company is able to negotiate with Ares in a smart way – probably in a year or so. This is because corporate credit spreads are extremely tight, and I believe that a Company of IEA’s size and quality would have no trouble refinancing the entire capital structure at 5-6% with a HY bond or a syndicated Term Loan facility. If we take into account the future cash interest savings, then the indifference point for paying the “make-whole” for the Preferred is not that far off. So in the next 12-18 months, the Company should approach Ares to negotiate the call protection down modestly so the economic arrangement makes sense for both parties, which would unlock the global refinancing.

Why would Ares ever entertain an arrangement like that, when the existing document is written in their favor? Well, from experience I know negotiations like this happen all the time – essentially what Ares is being asked to do is exchange some of the underwritten MOIC for additional IRR – a proposition that may well make sense in certain circumstances (e.g. are there attractive reinvestment opportunities elsewhere? Can this move optimize for their carry in the fund?). Also, there is a powerful economic incentive for Ares in the form of their ownership of the Common (through the penny warrants and anti-dilution shares) – which comes out to about 8mm shares on a fully diluted basis. If Ares agrees with the contention that a global refinancing is hugely value-accretive to the common equity (no-brainer) then they have the incentive to realize that value – for every $1 increase in the share price, Ares would be creating $8mm of incremental value for themselves.

Return Potential

Now let’s take a big step back – Ares may just tell the Company to pound sand, in which case we’d be stuck with the expensive Preferred until 2025 (or 2024 if taken out at 1.5x MOIC), but that’s not the end of the world. Consider the FCF profile for 2021 for instance – $135mm of EBITDA, $37mm of capex, $44mm of cash interest/dividend, no cash taxes (due to NOLs), implies $55mm of LFCF, excluding any swings in working capital. $55mm is a very healthy number – 11% of market cap assuming full dilution. For a company that should be growing FCF at healthy double digits annually, this seems far too generous to me – especially given that there is optionality for a refinancing down the road which would provide for a step-function increase in FCF when that eventually happens.

So what are we playing for, exactly? I gave this some thought, and I believe that if you give the Company 12-18 months to continue executing, I believe there is serious potential for EBITDA growth and multiple expansion as the Company capitalizes on macro tailwinds, and the story gets more widely disseminated. If you refer to the sensitivity table below, I feel comfortable playing for a 75 – 100% return from here. But my estimates may well prove conservative – sky is truly the limit if the ESG momentum & oil price go parabolic – and I think they just might.

Final Word

I hesitated before writing this last point, because I take pride in myself for being a fundamental value investor. But I do recognize that in a world awash with endless liquidity, technical dynamics can also be important… so screw it, here it is: IEA has a non-trivial chance of becoming a meme stock. It captures the ESG/renewables zeitgeist perfectly, and has a sizable following on Reddit boards and Stocktwits. It also has ~3mm shares sold short, which equates to 13% short interest, and definitely ripe for a short squeeze once the market figures out how attractive this stock is. Now, let’s be real – it is more likely that nothing crazy happens… but if there is an almighty spike one day… rest assured Plum Capital will take full credit for it.

Disclosure

Plum Capital is long IEA common stock

IEA is my own original idea, but the thesis magically formed in my head while I was listening to Harris Kupperman (aka Kuppy) during his segment on Market Huddle. I’ve been a religious listener for the past couple years, and I encourage everyone to check it out! Not only is the podcast great entertainment, the hosts (Patrick Ceresna and Kevin Muir) are super knowledgeable, and I always end up walking away with an investment idea or two from each episode.

Any updates or recent thoughts on IEA?

Will the $300mm debt raise take out the preferreds?